Financial Education

Posted on - 17th August, 2020 Posted by - Yallaschools

Paying for Tomorrow's Education Starts Today

Have you realised how funding a child’s education ends up teaching the parent a lesson in finance management?

It begins with primary and secondary education. As a parent, you want to send your child to the best schools, and this normally equates to higher school fees. Along with this comes costs related to transport, after-school activities, uniform, stationery and device expenses.

Some parents turn to banks to ease the financial burden with the help of credit cards as they offer installment plans at a low interest rate. However, to avoid mounting debt, parents should have a strong financial discipline when using credit cards to cover school fees.

Then, there is the challenge of higher education costs –the lack of funds shouldn’t come in the way of acknowledging your child’s dreams. To save effectively, It's Important you have a solid plan. Here are some simple steps to help you get started:

Step 1: Research the cost of education to get an estimate of eventual costs

Understanding the current cost of education depends on the level of education you want your child to get, and the type of college/university. Also, determine whether your child will study locally or abroad for graduate and post-graduate degrees and at which institutions.

Step 2: Determine the time horizon

For investments, time is the most crucial factor. A time horizon is the number of years you have left to save – between your child’s current age and when they start university.

Step 3: Consider the impact of inflation

Many studies across different countries have shown that the rise in cost of education has galloped past the rise in inflation. You need to factor in the rate of inflation in the country that you are considering.

Step 4: Pick a rate of return that you would need

Picking a reasonable rate of return on your investments is important. This rate should be higher than the rate of inflation so you can preserve the purchasing power of your money. E.g. A mutual fund could give a higher rate of return than fixed deposits. Although the rate of return may not be fixed, you can take an educated guess on the long-term returns of a moderately risky mutual fund – like the My Future Saver plan (an investment-linked insurance policy).

Step 5: Calculate the required monthly savings

Finally, with the expected rate of return and the final estimate, you can calculate the exact amount you need to save monthly. An online calculator can help figure out how much you will need to save every month.

Follow these 5 steps to calculate the exact amount of monthly savings you need to meet your child's higher education goal.

You can also talk to our Wealth Specialists to assist you further with your child’s education savings plan.

*****

Financial Education

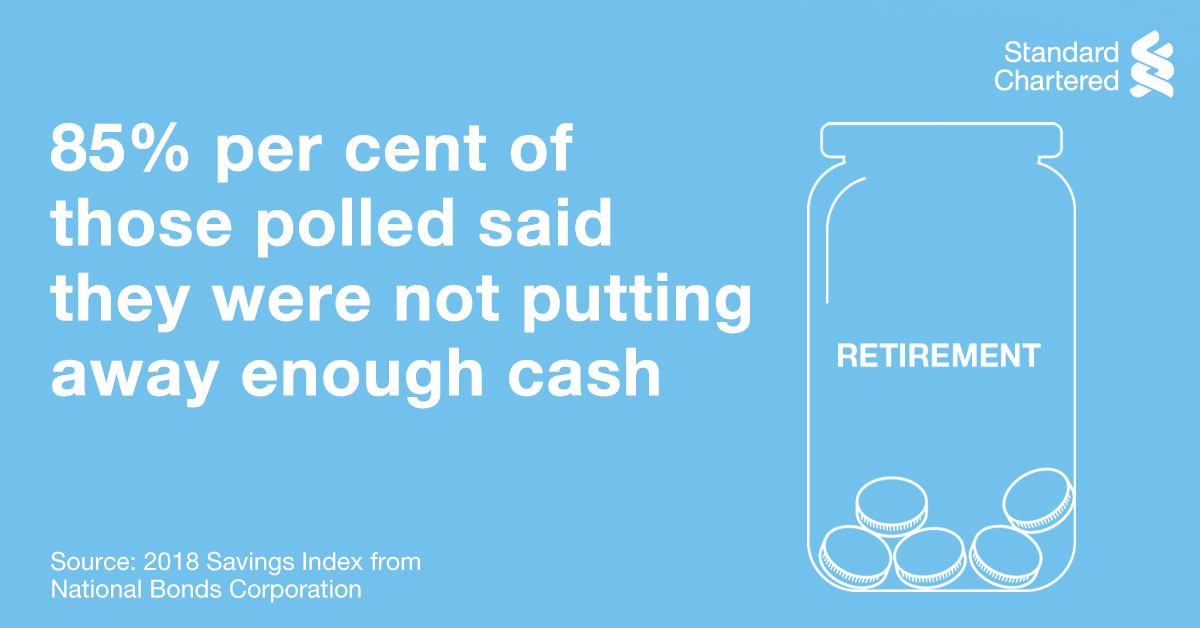

Saving For Retirement Starts Yesterday

Posted on - 18th November, 2020

Saving for retirement starts yesterday Here’s a wake-up call if you ever needed one. According to the 2018 Savings Index from National Bonds....

Financial Education

Make a confident step into your first home

Posted on - 6th October, 2020

Make a confident step into your first home There is a great sense of achievement when you buy your first home. You finally find one that fits your....

Financial Education

Paying for Tomorrow's Education Starts Today

Posted on - 17th August, 2020

Have you realised how funding a child’s education ends up teaching the parent a lesson in finance management? It begins with primary and secondary....

Financial Education

10 things I wish I knew about money when I was younger

Posted on - 27th July, 2020

.jpg)

10 things I wish I knew about money when I was younger Hindsight is a true gift. A lot of us look back to our early years and wish we’d done....

Financial Education

In An Emergency Use An Emergency Fund

Posted on - 9th June, 2020

If there’s one thing this period has taught us is that nothing is certain…especially one’s income. That’s why an emergency fund is....

Financial Education

Don’t Be A Victim, Watch out for Fraudsters

Posted on - 7th June, 2020

Don’t Be A Victim, Watch out for Fraudsters Cyber criminals are all around us, lurking in silence trying to steal your money and information. You....

Financial Education

Why everyone should have insurance?

Posted on - 19th May, 2020

People have car insurance, home insurance, travel insurance… but life insurance? Fact: Life is unpredictable. But we often ignore this,....

Financial Education

Schooling kids in money matters

Posted on - 8th March, 2020

We get it, school is expensive. And we are not even talking about school fees, extra-curriculars or after-school tuitions. We mean the daily expenses....

.jpg)

7th February, 2025 at 9:00 AM

International Career Counselors Conference and Awards 2025

Yallaschools.com

Venue: Dubai - UAE

1st June, 2025 at 10:45 AM

11th India Middle East Education Awards 2025 | Grand Awards

Yallaschools.com

Academic Excellence Awards

.jpg)

Amazing Career Counselor Awards

26th June, 2024

The Indian Curriculum Career Counselor Awards 2024 - Yearbook

Amazing Career Counselor Awards

18th June, 2024

Academic Excellence Awards

Academic Excellence Awards

_(1).jpg)

26th December, 2023

4th International Middle East 'AS Level' Education Grand Awards 2023

Academic Excellence Awards

.jpg)

.jpg) UAE

UAE Oman

Oman Bahrain

Bahrain KSA

KSA

Leave Your views & comments here

View More View Less