Financial Education

Posted on - 6th October, 2020 Posted by - Yallaschools

Make a confident step into your first home

Make a confident step into your first home

There is a great sense of achievement when you buy your first home. You finally find one that fits your budget and all you have to do is make the first deposit or down payment. This is no small amount and needs significant planning, in order to make one of your life’s ambitions a reality for you and your children.

Assess your financial position

Evaluate your income versus your living expenses and any debt you have, then work out how much of your monthly income can be diverted towards mortgage repayments. You may speak to the mortgage advisor at the bank offering the lowest rate for you to know how much you can borrow. Once you know how much you can borrow, you will know the value of the property you can afford and, in turn, how much deposit/down payment you need. In the UAE, expats need to make a cash down payment of at least 20% of the property value.

Factor in all costs

Remember, you are not just saving for the deposit/down payment, but also any fees such as valuation, surveyor, brokerage charges as well as property transfer and mortgage application fees. Other overlooked costs include the cost of moving as well as connection fees for utilities. Add these to your target figure and then you’ll know how much you need to save.

Use your savings account strategically

It’s good to maintain a separate savings account and commit not to withdraw from it unless it’s for the first deposit. Setting up a standing order from your bank account into your down payment fund is a key way to make sure the money is transferred without you having to think about it. The more you save in this account the better, as it reduces the monthly payments you make on your mortgage. Be aware that not all savings accounts are the same. Besides interest rates, there can be a huge variety in terms of how you access your money.

Investments

While keeping money in your savings account is less risky, you can obtain better appreciation for it when you invest in medium-risk mutual funds. Markets are volatile and it’s worth speaking to a professional financial advisor to discuss your risk levels and find an opportunity that is right for you.

Maintain a budget

Living within a budget is an evergreen tool when it comes to savings and investments. The golden rule of a budget is that your income should always be greater than expenses. Since you are saving up for a home, your expenses must factor in the amount you are committed to saving every month. Keep a watchful eye on your utility bills, as well as entertainment and dining out. These small sacrifices will pay off in the long run.

Finally, if your dream home is out of your reach, save for a less expensive property. You can then build up equity as the market rises and later sell it to buy a bigger home. Your dreams don’t have to be put on hold and Standard Chartered is here to help you achieve them. For guidance on saving for your first home, reach out to one of our Wealth Specialists.

**************

Financial Education

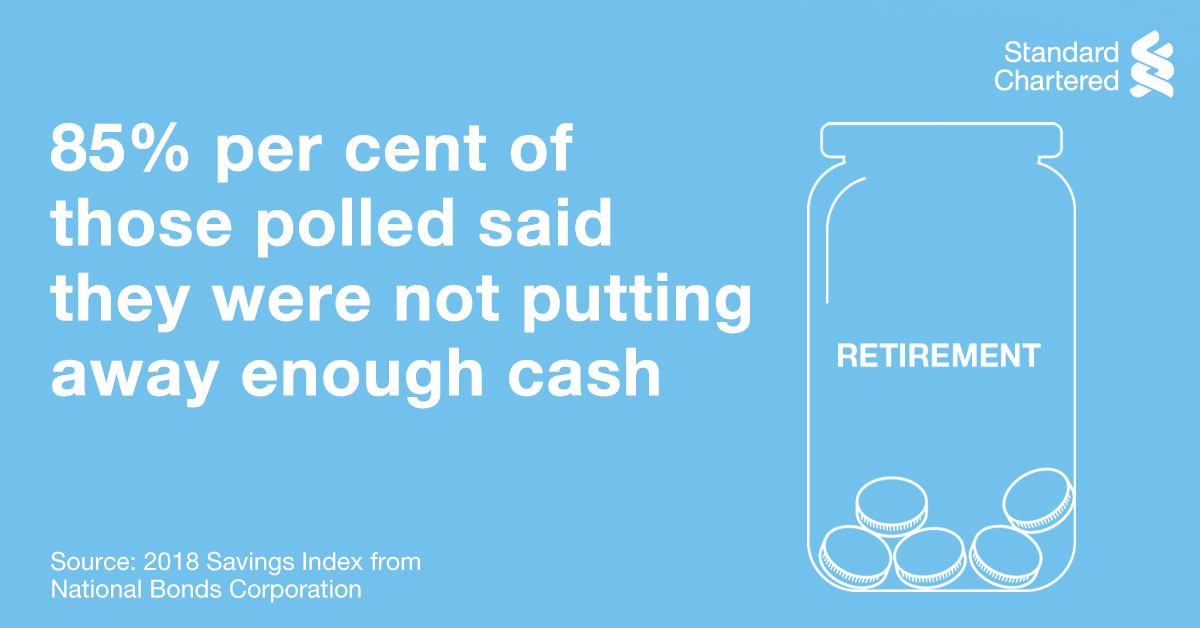

Saving For Retirement Starts Yesterday

Posted on - 18th November, 2020

Saving for retirement starts yesterday Here’s a wake-up call if you ever needed one. According to the 2018 Savings Index from National Bonds....

Financial Education

Make a confident step into your first home

Posted on - 6th October, 2020

Make a confident step into your first home There is a great sense of achievement when you buy your first home. You finally find one that fits your....

Financial Education

Paying for Tomorrow's Education Starts Today

Posted on - 17th August, 2020

Have you realised how funding a child’s education ends up teaching the parent a lesson in finance management? It begins with primary and secondary....

Financial Education

10 things I wish I knew about money when I was younger

Posted on - 27th July, 2020

.jpg)

10 things I wish I knew about money when I was younger Hindsight is a true gift. A lot of us look back to our early years and wish we’d done....

Financial Education

In An Emergency Use An Emergency Fund

Posted on - 9th June, 2020

If there’s one thing this period has taught us is that nothing is certain…especially one’s income. That’s why an emergency fund is....

Financial Education

Don’t Be A Victim, Watch out for Fraudsters

Posted on - 7th June, 2020

Don’t Be A Victim, Watch out for Fraudsters Cyber criminals are all around us, lurking in silence trying to steal your money and information. You....

Financial Education

Why everyone should have insurance?

Posted on - 19th May, 2020

People have car insurance, home insurance, travel insurance… but life insurance? Fact: Life is unpredictable. But we often ignore this,....

Financial Education

Schooling kids in money matters

Posted on - 8th March, 2020

We get it, school is expensive. And we are not even talking about school fees, extra-curriculars or after-school tuitions. We mean the daily expenses....

.jpg)

7th February, 2025 at 9:00 AM

International Career Counselors Conference and Awards 2025

Yallaschools.com

Venue: Dubai - UAE

1st June, 2025 at 10:45 AM

11th India Middle East Education Awards 2025 | Grand Awards

Yallaschools.com

Academic Excellence Awards

.jpg)

Amazing Career Counselor Awards

26th June, 2024

The Indian Curriculum Career Counselor Awards 2024 - Yearbook

Amazing Career Counselor Awards

18th June, 2024

Academic Excellence Awards

Academic Excellence Awards

.jpg)

26th December, 2023

4th International Middle East 'AS Level' Education Grand Awards 2023

Academic Excellence Awards

.jpg)

.jpg) UAE

UAE Oman

Oman Bahrain

Bahrain KSA

KSA

Leave Your views & comments here

View More View Less